400km Hydrogen Pipeline With No Users Will Raise Germany’s Electricity Prices

Germany recently completed and pressurized the first roughly 400km segment of its national hydrogen backbone. The pipes are in the ground, the compressors work, and the system is technically ready. There is only one problem. There are no meaningful hydrogen suppliers connected and no material customers contracted. This is not a commissioning delay or a temporary mismatch. It is a structural failure of demand. The reason this matters far beyond hydrogen policy is simple. The cost of this infrastructure will not disappear. It will persist for decades and will be paid for through higher electricity bills.

The original intent behind Germany’s hydrogen backbone was straightforward and politically appealing. Hydrogen was framed as a future energy carrier that would replace natural gas across multiple sectors. A national transmission network of around 9,000km was proposed, with individual corridors sized at 10GW to 20GW. The idea was to build the infrastructure first and allow supply and demand to follow. Hydrogen would serve steel, chemicals, transport fuels, dispatchable power generation, and heavy industry. In policy documents and commissioned studies, hydrogen demand rose quickly into the 100 TWh to 130 TWh range by 2030 and beyond. At that scale, a national backbone looked reasonable.

As a note on the choice of units which is supporting a lot of bad assumptions about hydrogen, let’s look at the choice to use TWh by Germany. At hydrogen’s lower heating value, 1 kg of hydrogen contains about 33.3 kWh of usable chemical energy, with the lower heating value convention meaning the latent heat in the water vapor formed during combustion is not counted because most real systems do not recover it. On that basis, 1 TWh of hydrogen corresponds to about 30,000 tons of hydrogen.

One recurring analytical error I have highlighted in European hydrogen policy is the persistent misuse of energy units to describe what is fundamentally a material flow problem. Hydrogen is not electricity. It is an industrial feedstock measured and traded in kilograms and tons, yet European strategies repeatedly describe hydrogen demand and infrastructure in TWh, borrowing the language of power systems and gas grids. This unit choice embeds a false analogy, implying hydrogen is a fungible energy carrier moving through the economy like electrons. It obscures mass balance constraints, hides volumetric and compression penalties, and makes pipelines appear comparable to transmission lines.

A further distinction often missed in hydrogen modeling is the difference between a TWh of delivered electricity to a load and a TWh of delivered hydrogen. A TWh of electricity arrives at a customer meter with transmission and distribution losses typically around 5% to 8%, and nearly all of that energy can be converted directly into useful heat or work. A TWh of hydrogen, by contrast, represents chemical energy after a long chain of losses. Producing that hydrogen via electrolysis typically consumes about 1.5 TWh of electricity. Compressing it to pipeline pressures, storing it, and distributing it erodes another 5% to 15%.

If the hydrogen is then used for heating, combustion losses mean that less useful heat reaches the end use than direct electric heating would have delivered from the original electricity. If the hydrogen is used to perform work, such as moving a vehicle, the losses multiply. Fuel cells or engines convert only a fraction of the hydrogen’s chemical energy into motion, leaving overall electricity to wheels efficiency commonly below 30%. In practical terms, a TWh of electricity delivers close to a TWh of service, while a TWh of hydrogen often represents two to three TWh of upstream electricity consumed to deliver the same or less useful outcome. Using TWh embeds the primary energy fallacy in German and European energy policy.

When hydrogen demand is expressed in tons, it is immediately placed in its proper category as an industrial material rather than an energy flow. Germany’s realistic end state hydrogen requirement is a few hundred thousand tons per year, which is comparable to other specialized chemical feedstocks and entirely inconsistent with the scale implied by national energy infrastructure. Framed this way, hydrogen looks like something to be produced where it is cheapest, shipped where it is needed—likely in intermediate products such as hot briquetted iron, ammonia and methanol—and used sparingly in specific processes, not something that warrants a country-spanning transmission network. When the same quantities are expressed in TWh, they encouraging planners to think in terms of power systems and pipelines rather than chemistry and supply chains. This unit choice inflated perceived scale, blurred the distinction between energy and material use, and helped justify a hydrogen backbone that only makes sense if hydrogen is misclassified as a general energy commodity.

The direct problem is that none of the hydrogen volume assumptions, regardless of units, survive contact with physics, economics, or observed market behavior. Start with supply. Germany is not a low cost electricity jurisdiction. Industrial power prices have been persistently high relative to most of the world, and electrolysis only converts electricity into hydrogen with losses. Even optimistic system assumptions require 50kWh to 55kWh of electricity per kilogram of hydrogen. At German power prices, domestic green hydrogen struggles to compete with imports even before compression, storage, and distribution costs are included. Electrolyser buildout has lagged targets, and there is no credible path to producing tens of TWh of hydrogen domestically at competitive cost.

Imports were supposed to close the gap. Ports such as Rostock and Wilhelmshaven were highlighted as gateways for hydrogen and hydrogen derivatives. In practice, exporters prefer to ship finished molecules such as ammonia, methanol, or iron products rather than gaseous hydrogen. Dedicated hydrogen pipelines from other countries have been delayed, resized, or quietly abandoned when buyers declined to sign contracts at required prices. Germany built transmission capacity before securing supply at scale, and the suppliers did not appear.

The demand side is where the strategy truly collapses. Oil refining has historically been Germany’s largest hydrogen consumer, using roughly 25 TWh to 30 TWh—750,000 to 900,000 tons—per year for hydrocracking and desulfurization. That demand exists only because Germany refines fossil fuels. In any credible decarbonization pathway, fuel refining declines steadily and eventually disappears. In an end state with no refined fossil fuels, refinery hydrogen demand goes to zero. There is no offsetting growth from petrochemicals, because German refineries are fuel oriented. About 85% to 90% of crude oil processed in Germany becomes fuels, not chemical feedstocks.

Petrochemicals remain, but their hydrogen demand is far smaller than often implied. Steam crackers do not consume hydrogen. They typically produce hydrogen as a byproduct, on the order of 1.5% to 3% of feed by mass. Some hydrogen is required for selective hydrogenation and purification steps in aromatics and specialty chemicals, but the quantities are bounded. A conservative upper estimate is 5 kg to 10 kg of hydrogen per ton of petrochemical product. Applied to Germany’s chemical output, that yields roughly 4 TWh to 8 TWh—120,000 to 240,000 tons—of hydrogen demand. This is the largest durable hydrogen use case in a fuel free Germany, and it is an order of magnitude smaller than what backbone planners assumed.

Ammonia is often presented as another anchor customer for domestic hydrogen, but the economics point in a different direction. Ammonia production in Germany has already shown how exposed it is to energy prices, with plants shutting down or idling during periods of high electricity and gas costs. What Germany is competitive at is not bulk ammonia synthesis, but the downstream, higher value manufacturing that uses ammonia as an intermediate, including fertilizers, nitric acid, and specialty chemical products. In a realistic end state, Germany would import green ammonia from regions with abundant low cost electricity and established export logistics, then convert that ammonia domestically into higher value derivatives close to end markets. This preserves industrial employment and value creation while minimizing energy system costs. Under this model, domestic hydrogen demand for ammonia synthesis largely disappears, aside from a few niche or transitional facilities, and treating ammonia as a stable domestic hydrogen sink misreads how chemical value chains and trade actually function.

Steel is the centerpiece of Germany’s hydrogen narrative and one of its many weak links. Strategy documents assume roughly 14 million tons to 15 million tons of domestic hydrogen based direct reduced iron capacity by 2030, corresponding to about 28 TWh to 29 TWh—840,000 to 870,000 tons—of hydrogen demand. This assumes that German steelmakers will run large DRI modules on green hydrogen produced or delivered domestically. That assumption fails on several fronts. Germany already produces about 35 million tons to 37 million tons of crude steel per year while consuming only about 26 million tons to 27 million tons domestically. The rest is exported into competitive global markets. Cost matters.

Germany currently produces about one third of its steel in electric arc furnaces. The United States operates at roughly 71% EAF. Germany cannot reach that level because of product mix and residual contamination limits, but it can plausibly reach 45% to 55% EAF using better scrap sorting and blending. That shift alone displaces a large share of primary steelmaking without any hydrogen. The remaining need for clean iron units is best met by importing hot briquetted iron produced where electricity is cheap, or by using biomethane based DRI domestically before hydrogen based DRI. Biomethane with carbon capture produces a concentrated biogenic CO2 stream for sequestration and avoids hydrogen entirely. Under this rational pathway, domestic hydrogen demand for steel goes to zero.

That upper bound of roughly 55% EAF is not necessarily permanent, by the way, but it is a realistic constraint under today’s conditions of scrap quality and product mix. Germany’s limitation is not conceptual but material. Its scrap stream is more contaminated and its steel demand skews toward high end flat and precision products. Over time, both of those constraints could soften. One pathway is active scrap triage, where the most copper and tin contaminated scrap is deliberately separated and exported, while the cleanest scrap fractions are retained for domestic EAF use. That approach treats scrap quality as a strategic resource rather than a homogeneous waste stream. Another pathway is the eventual commercialization of impurity removal processes that are currently confined to laboratories or pilot plants. As imported green iron units will remain structurally expensive relative to fossil iron, and as carbon pricing tightens further, processes that selectively remove copper or other residuals from scrap would become competitive at the margin. If either or both of these developments materialize, Germany could push scrap based EAF production beyond today’s plausible ceiling, and Germany should adopt this strategy. For now, however, that ceiling reflects present economics and metallurgy, not an immutable physical limit.

Transport was another major projected demand wedge. In reality, battery electric vehicles dominate road transport on cost and efficiency. Hydrogen trucks have failed to scale and are being abandoned, while battery electric trucks are taking market share. Hydrogen trains are dead, with Alstom leaving the space entirely and German transit agencies ditching their hydrogen plans. Aviation and shipping fuels, where hydrogen appears indirectly as a biofuel hydrotreater, are imported molecules. Germany is not going to produce e fuels domestically at scale using high priced electricity, and e fuels will have at best a niche play to fill in any biofuels gaps. Setting transport and e fuels to zero domestic hydrogen demand is not aggressive. It reflects market outcomes already visible.

Power generation is often cited as a future hydrogen sink through hydrogen ready gas plants. Capacity is not demand. A plant that runs a few hundred hours per year as insurance does not consume TWh of fuel. Hydrogen is an expensive way to provide dispatchable power compared to batteries, grids, and demand response. Annual hydrogen consumption for power in Germany is likely measured in fractions of a TWh, if it exists at all.

When all of these sectors are examined honestly, Germany’s realistic steady state hydrogen demand collapses. Instead of 110 TWh to 130 TWh, the number is about 4 TWh to 14 TWh—120,000 to 420,000 tons—, with the lower end representing petrochemicals only and the upper end including residual ammonia or niche uses. Using the midpoint, Germany needs roughly 0.5 GW to 1 GW of continuous hydrogen flow. Even allowing for peaks, 2 GW covers the system, but buffering with storage would be more reasonable than a 2 GW pipeline.

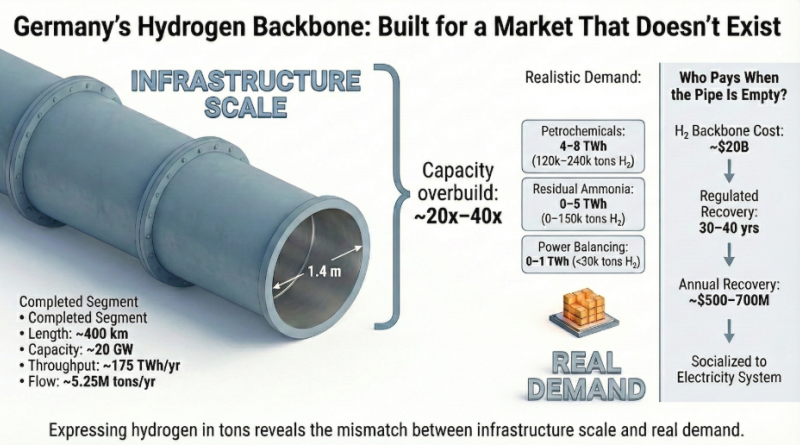

Now compare that to the hydrogen backbone that is being built. The commissioned 400km segment alone is framed as having around 20 GW of capacity. At full utilization, that corresponds to roughly 175 TWh—5.25 million tons—per year. Against a realistic demand of 4 TWh to 8 TWh, this is an overbuild of about 22x to 44x. Even against generous peak assumptions, the system is scaled an order of magnitude too large. This is not a rounding error. It is a fundamental mismatch between infrastructure and need.

Germany’s hydrogen backbone also bakes in a severe unit cost problem that is temporarily hidden by subsidized ramp-up tariffs at the start of the pipeline’s lifetime. In the early years, hydrogen network charges are deliberately set well below full cost recovery to make hydrogen appear affordable to hypothetical users, with the shortfall deferred and socialized through the regulatory asset base. This creates the impression that transport costs are modest, but it is an accounting artifact, not an economic reality. Even with the artificially low transportation charges, there are no takers because production remains expensive. The core network is expected to require on the order of $500 million to $700 million per year to recover capital and regulated returns.

At the designed utilization of roughly 175 TWh per year, equivalent to about 5.25 million tons of hydrogen, that would translate into a network cost of roughly $0.10 to $0.15 per kg. That benign figure is implicitly assumed in strategy documents. In the realistic end state, however, Germany’s domestic hydrogen demand is closer to 120,000 to 240,000 tons per year. Spread across that volume, the same fixed network costs rise to roughly $2 to $5 per kg of hydrogen, before production, compression, storage, or distribution are counted. The initial subsidy merely postpones this outcome. As the deferred costs are eventually recovered, the roughly 44x mismatch between designed capacity and actual usage ensures that pipeline transport becomes prohibitively expensive per unit, reinforcing weak demand and locking in a long-term subsidy burden that electricity consumers must carry for decades.

The financial implications follow from Germany’s regulatory model. Hydrogen pipelines are treated as regulated assets. Transmission system operators finance construction with debt and equity and place the assets into the regulated asset base. They earn an allowed return and recover depreciation over 30 to 40 years. Utilization is not required for cost recovery. During the ramp up period, hydrogen tariffs are deliberately set below cost to attract hypothetical users. The shortfall is accumulated and socialized.

When hydrogen demand does not materialize, the pipes are not written off. There is no stranding trigger. The assets are considered used because they are available. With few hydrogen customers to pay tariffs, costs are shifted across the wider energy system. In practice, this means electricity network charges, levies, and federal budget transfers funded by taxpayers and electricity consumers.

The core hydrogen network is estimated to cost about $20 billion. Spread over 40 years, annualized recovery including returns is on the order of $500 million to $700 million per year. Germany consumes about 500 TWh of electricity annually. Socialized across electricity users, this adds roughly $1 to $1.5 per MWh, or about $0.001 to $0.0015 per kWh. On its own, this looks modest. It is not isolated. It stacks on top of other fixed system costs and raises the baseline price of electricity for decades.

The more important effect is opportunity cost. $20 billion invested in grid reinforcement, wind, solar, storage, and flexibility would lower wholesale prices, reduce congestion, and speed electrification. Locked into underused pipelines, that capital instead earns regulated returns while delivering no economic value. The result is higher electricity prices than necessary, which slows adoption of heat pumps, electric vehicles, and industrial electrification. Hydrogen overbuild indirectly undermines the energy transition it was supposed to support.

None of this was unpredictable, but was a complete failure of technoeconomic analysis and governance in Germany. In reviewing Germany’s hydrogen assumptions, I examined work from organizations that are widely treated as authoritative in research and policy analysis, including Fraunhofer institutes, Agora Energiewende, Deutsche Energie-Agentur (dena), the Potsdam Institute for Climate Impact Research (PKI), European Commission modeling groups, and consultancies such as DNV working closely with gas transmission operators.

When reviewing the studies, a consistent pattern emerged. Hydrogen prices were routinely assumed to fall to levels that were disconnected from physical reality, often based on optimistic electrolyser learning curves while quietly excluding the costs of compression to pipeline pressures, storage losses, boil off, reconversion, and distribution. Electricity input prices were frequently taken from best hour renewable scenarios rather than system average prices, even though electrolysers require high utilization to be economical. In parallel, demand was rarely grounded in signed contracts or credible purchasing behavior. Instead, models treated hydrogen demand as an outcome of policy intent, assuming that if infrastructure existed, industry would adapt its processes regardless of cost. This inverted causality allowed demand to be assumed into existence rather than earned through competitiveness.

In one memorable case, a bar chart included in a report from PKI had the cost of energy for green hydrogen at half the cost per MWh of the cost of the electricity used to create it, an energetically impossible outcome, yet none of the researchers involved or reviewers of the paper noticed the massive and glaring discrepancy. Instead, the researchers assumed that they had entered the correct numbers for electricity and that the hydrogen would therefore adjust, not realizing that unrealistically low hydrogen prices were hard coded in the models.

A second recurring issue was institutional bias. Gas transmission operators and their affiliated research partners were deeply embedded in scenario development, and unsurprisingly produced pathways in which repurposed gas pipelines became hydrogen backbones. These studies often compared hydrogen transmission to electricity transmission using energy units, masking volumetric inefficiencies and reinforcing the false equivalence between moving electrons and moving molecules. Hydrogen was framed as a system wide energy carrier rather than a constrained chemical input, which inflated perceived scale and justified national infrastructure. Steel, transport, and power generation demand were repeatedly overstated by assuming hydrogen would be chosen even where simpler electrified alternatives were already cheaper or clearly trending that way.

Perhaps most striking was that these assumptions did not converge toward reality over time. As evidence accumulated that hydrogen trucks were failing, that industrial offtakers were unwilling to sign long term contracts at required prices, and that electrolyser projects were stalling, the models were not revised in kind. Instead, new reports recycled similar assumptions with minor parameter tweaks, reinforcing the same conclusions. The analytical errors were not hidden or technical. They were structural and visible to anyone checking mass balances, cost stacks, or trade dynamics. Those critiques were published, debated, and dismissed. Germany did not lack warning signals. It chose to proceed anyway, and the consequences are now embedded in steel, concrete, and regulated assets that will shape electricity costs for decades.

The deeper failure is conceptual. Hydrogen makes sense where chemistry requires it. It performs poorly as a way to move or store energy compared to moving electrons directly. Germany blurred that distinction, built policy around the blur, and then committed capital at national scale. The result is a pressurized pipeline with no molecules, no customers, and a long tail of costs.

Germany still has a choice. It can stop expanding the hydrogen backbone now, before more capital is sunk into assets that will never be used economically. It can right size hydrogen infrastructure to regional industrial gas networks measured in single digit GW, not national energy corridors. It can redirect investment toward the electricity system, where decarbonization actually happens. If it does not, electricity consumers will keep paying for a hydrogen fantasy that never matched reality.

Cover photo: Google Gemini generated this infographic illustrating the stark mismatch between the massive scale of Germany's planned hydrogen infrastructure and current realistic demand.