The urgent case for green finance.

Existing sources of capital will not suffice to tackle climate change concerns. Here’s what needs to be done.

Mumbai: A silent revolution is taking place, one which we cannot ignore. Climate change has been thrust into the foreground of the public consciousness and institutional investors are under pressure to act. This year’s annual general meeting of BP Plc signalled this shift quite unabashedly. While protesters lined the streets outside, a number of institutional investors, including Aviva Investors and Hermes Investment Management, stood up inside the room to voice the same climate concerns.

Clearly, tackling climate change has become a necessity. The financial sector has to develop approaches and instruments in order to make environmental finance a mainstream priority. In order to counter the impact of climate change, India needs massive capital. The environment ministry estimates that India will need $2.5 trillion to meet climate change targets, of which $280 billion is needed in the next five years for green infrastructure alone. The size of investments estimated is not something India has ever managed before, considering the country’s total investments in infrastructure has been just over $1 trillion in the previous decade and a half.

To understand the enormity of the challenge ahead, consider just one recent example: India is aiming big in the electric vehicle (EV) space, offering a slew of incentives. NITI Aayog has set an ambitious target of 40-80% EV penetration in different consumer segments, but this would entail creating the adequate charging infrastructure and investments in storage technologies to reduce upfront costs. The government has plans to build Tesla-style gigafactories in India, which will cost approximately $5 billion. All these plans will require green finance at an affordable cost.

To put it in perspective, India needs roughly three times the total investment made in the infrastructure sector in the last 10 years to tackle climate change for this decade. Existing sources of capital will simply not be adequate.

The challenge

Green finance—investments that have a positive impact on environment or reduce the risk of climate change—is the need of the moment. According to Dhanpal Jhaveri, chief executive of EverSource Capital, which is looking to invest $1 billion in India via its Green Growth Equity Fund, mainstreaming of green finance is an urgent requirement. “Air and water are the two most precious resources that we need to protect, not only for our current but also for our future generations," he says.

Integrating the needs of the environment into investor decision-making will make capital more likely to flow to assets that are compatible with sustainability. Doing so will also help financial institutions appropriately manage risk, improving the resilience of the financial system as a whole. According to Sandeep Bhattacharya of the Climate Bonds Initiative: “The end objective would be that nearly all financial transactions are green and thus ‘green’ from green finance drops off."

Cost is an important factor because traditional wisdom suggests that green investments come at the expense of growth, and hence, developing economies focus on reducing the cost of investments to spur growth. The genesis of this argument can be traced back to an inverse relationship between economic growth and environmental impact established by John Holdren and Paul Ehrlich in the 1970s.

The equation showed that with a rising population and (given economic growth) rising consumption, environmental impact would inevitably increase unless the rate of technological improvement was sufficient to overcome it. In India, both population and consumption are rising and this will lead to negative impact on environment. However, increased investments in green technology can offset this impact.

Consider this: A decade ago conventional thermal power was priced at 3.4 pence/kilowatt hour (kWh) compared to renewable power at 19 pence/kWh. And 10 years on, conventional power is priced at 5.1 pence/kWh compared to renewable energy at 3 pence/kWh, and returns in renewable are comparable, if not better, than the conventional space.

The big idea

According to experts, decisive action, both at the policy and market level, will help in gaining momentum. Such action could include the pricing of climate-related risks, mobilizing finance, and ensuring that there exist sound underlying policies.

The UK, which has emerged as the leading market for green finance, has set up a Green Finance Taskforce, a joint effort of the UK government and the City of London. The task force designs the overall roadmap for promoting green finance, advocates necessary policy and regulatory changes, and promotes the City of London as a green finance hub. And concerted effort from the task force has led to success—the London Stock Exchange (LSE) has emerged the most sought after green bond market.

According to Shrey Kohli, director, fixed income and funds, LSE, a total of 114 green bonds have been issued on the LSE from 44 issuers in 13 currencies and a total of $36 billion of green bonds have been raised, including some landmark issues by China, India, the Pacific (Fiji), Latin America (Chile) and the Middle East.

There are some simple steps that India can take to start a local green finance ecosystem. For one, to generate awareness and coordinate efforts, the Indian government, through NITI Aayog, can create a green finance strategy. “A green strategy is essential to coordinate among policymakers, regulators, institutional investors, and consumers. Awareness, understanding, and availability of green investment options over alternatives will be key," said Sambitosh Mohapatra, partner, PwC.

Alternate sources of capital

A fragile banking sector, a nascent corporate bond market, and a restrictive and expensive overseas borrowing route poses challenge for India to meet its “green" ambitions. India needs to leverage alternate sources of capital by either tapping into new sources of capital or by reducing restrictions on existing sources of capital. Pension funds, insurance companies, and retail investors cannot invest in private debt due to investment restrictions. These restrictions should be reduced, and such funds should be encouraged to invest in clean technology through time-bound incentives.

Encouraging non-resident Indians (NRIs) to invest in the clean technology space will open a large pool of capital. In order to nudge more overseas NRI capital into green finance, the government will need to ease foreign portfolio investment and repatriation policies—at least for green finance. Increased financialization can also benefit the green finance ecosystem by creating more demand for green products and services.

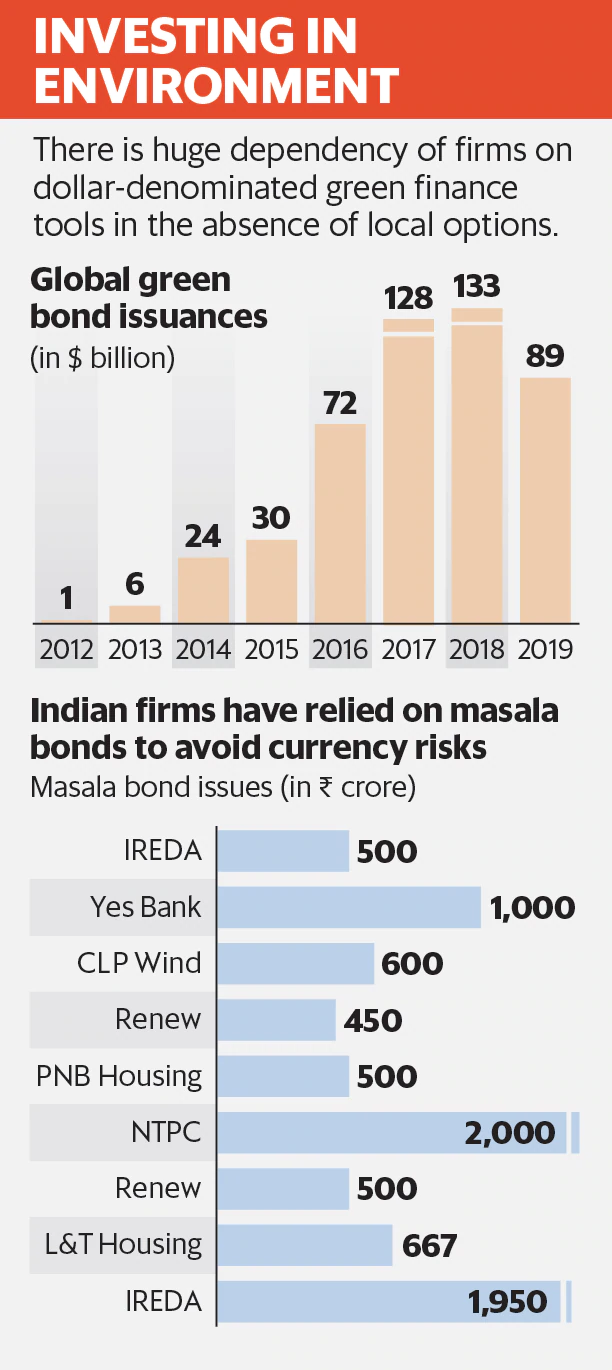

Finally, there is a need to have deeper capital markets. According to Jhaveri, mainstreaming green finance in capital markets, especially debt, has been a challenge in India so far. One of the most widely used green finance instrument today is green bonds, in which the proceeds are raised via bonds and the end use of the funds is clearly specified. Most Indian firms turn to the LSE to raise funds through green bonds. Renewable energy firms (such as Azure, NTPC, Greenko and Renew Power) and banks (such as Yes Bank, EXIM, L&T Finance, Axis, IDBI and REC) have issued green bonds on the LSE.

The challenge for most Indian firms is that the cost of issues is 5-6% per annum (post underwriting) and the cost of hedging for currency risk is roughly 3-4%. Thus, the net cost for the Indian borrower is in the similar range as domestic interest rates charged by commercial banks. As a result, some public entities, such as NTPC and Kerala Infrastructure Investment Fund Board, have issued green masala bonds, that are Rupee denominated green bonds at a rate of return of roughly 7.5%.

To reduce the cost of hedging, the government can create a dedicated fund to provide hedging services at less cost or reducing the risk of underlying investments by providing partial guarantees.

Guarantees from the public sector can be in the form of full or partial debt repayment to investors (e.g. the US Department of Energy Loan Guarantee Program) or in the form of insurance to equity investors (e.g. the Multilateral Investment Guarantee Agency’s (MIGA) political risk insurance).

They help mobilize private resources without requiring an immediate disbursement of financial resources from public budgets.

The green agenda

Indian firms are among the leading issuers of green bonds, raising about £5 billion, but the momentum is slowing down. Some steps have been taken—green bond guidelines by the Sebi and launch of a separate platform for issuing green bonds—but many more are needed. Corporates are often deterred by high transaction costs, taxes and stamp duties in India.

Here’s how one can change this status quo: Reducing incidental expenses for green bonds will encourage clean tech firms to leverage markets. Fiscal and tax incentives for clean tech will be an added advantage. The restriction on long-term sources of capital (like on pension and insurance funds) have to be relaxed for green financing. To safeguard the interest of such funds, governance around credit rating of bond issues needs to be strengthened. At the same time, green bonds could be opened up for retail participation. Opening up the bond market will need a more robust rating system that is not only able to identify the risk of an issue but also the degree of “green" component in the issue. This will help investors differentiate between green vs. brown assets. Finally, the government will have to create an Indian Space Research Organisation-like body for green technologies that focuses not only on innovation but also on commercialization of innovation.

In conclusion

It is good to “go green" but it also involves investment and extensive transformation in business as usual. As India changes the way products are made or packaged, favouring eco-friendly options and adopting new technologies to meet sustainability, the new targets can involve high cost and risk. The temptation to greenwash may rise. It is important to ensure governance in labelling and verification process to avoid such an eventuality. India has started to walk the talk on green finance through initiatives like India INX—India’s first international exchange—launched by BSE on which green bonds worth $ 4.1 billion have been listed. But we need to be faster in response, and steadier in our commitment to win this race against the risks from climate change.

11 August 2019

live mint